Sophisticated Strategy or Illegal Manipulation?

Jane Street Matter and the Indian law on Unilateral Manipulation of Scrip Prices through Market Trades

I. Introduction

The Jane Street Interim Order on manipulation of stock prices is slotted for appeal on the 9th of September 2025. What is “manipulation of price”, however? Can we legally define manipulation satisfactorily? What is an “artificial price” as against a “natural price” or a “market price”? What are the legal lines? In this article, I examine some of these questions in the context of Indian law on manipulation. In light of the law discussed, I briefly review the merits of SEBI’s case against Jane Street. I leave out the case for blatant misinformation, like a promoter of the company misrepresenting prospects or front-running by virtue of insider training and so forth, to focus solely on the manipulation of price through trading activity alone.

Summary

This article examines the legal framework governing stock price manipulation in India, focusing on the SEBI (Prohibition of Fraudulent and Unfair Trade Practices) Regulations, 2003. With the Jane Street interim order appeal scheduled for September 9, 2025, the paper delves into the core definitional challenge of distinguishing an "artificial price" from a legitimate "market price." Through a thematic analysis of key precedents from the Securities Appellate Tribunal (SAT) and the Supreme Court of India, the article identifies the evolving legal tests for manipulation, including those related to intent, trading patterns, and unilateral schemes. These established principles are then applied to the facts of the Jane Street case, which involves a complex, cross-market strategy. The analysis concludes that SEBI has a formidable legal case, and the appeal's outcome will be a landmark decision for the regulation of sophisticated, quantitative trading strategies in Indian capital markets.

Table of Contents

III. What is “Manipulation” of Scrip Prices?

IV. Some Economic Thinking on “Price”

VI. Tentative Facts entering the Determination of Manipulation

VII. Intention of the Party to Manipulate Price

IX. Jane Street Group Interim Order

X. Legal Position qua Jane Street Allegations

II. Statutory scheme

S. 3 and S. 4 of the SEBI (Prohibition of Fraudulent and Unfair Trade Practices relating to Securities Market) Regulations, 2003[1] (PFTUPR for short) govern “manipulative, fraudulent and unfair” trade practices in the securities market. The definitions in these regulations, as in most PFUTP regulations elsewhere, are wide and vague.

For instance, consider S. 3(d): This provision prohibits as manipulative, “any direct or indirect practice or course of business that operates as fraud or deceit in the issue, dealing in or trading of securities listed or proposed to be listed”. SEBI exercises abundant discretion in determining whether an instance or act was manipulative or deceitful.

Further, the definition of Fraud [see below] in the regulations is widened in scope substantially as against the traditional understanding of Fraud. Fraud in PFUTP includes misrepresentation and even silence qua material facts. Intention requirements in Fraud, to either defraud or to make gains or to avoid losses, are relaxed substantially, too, as we shall see in the sections that follow. In dealing with securities in India, the duty imposed on persons dealing with securities therefore approaches a very high standard akin to utmost good faith. The regulations sanction almost all acts or omissions in the disclosure of information and fidelity of transactions through widely drafted language.

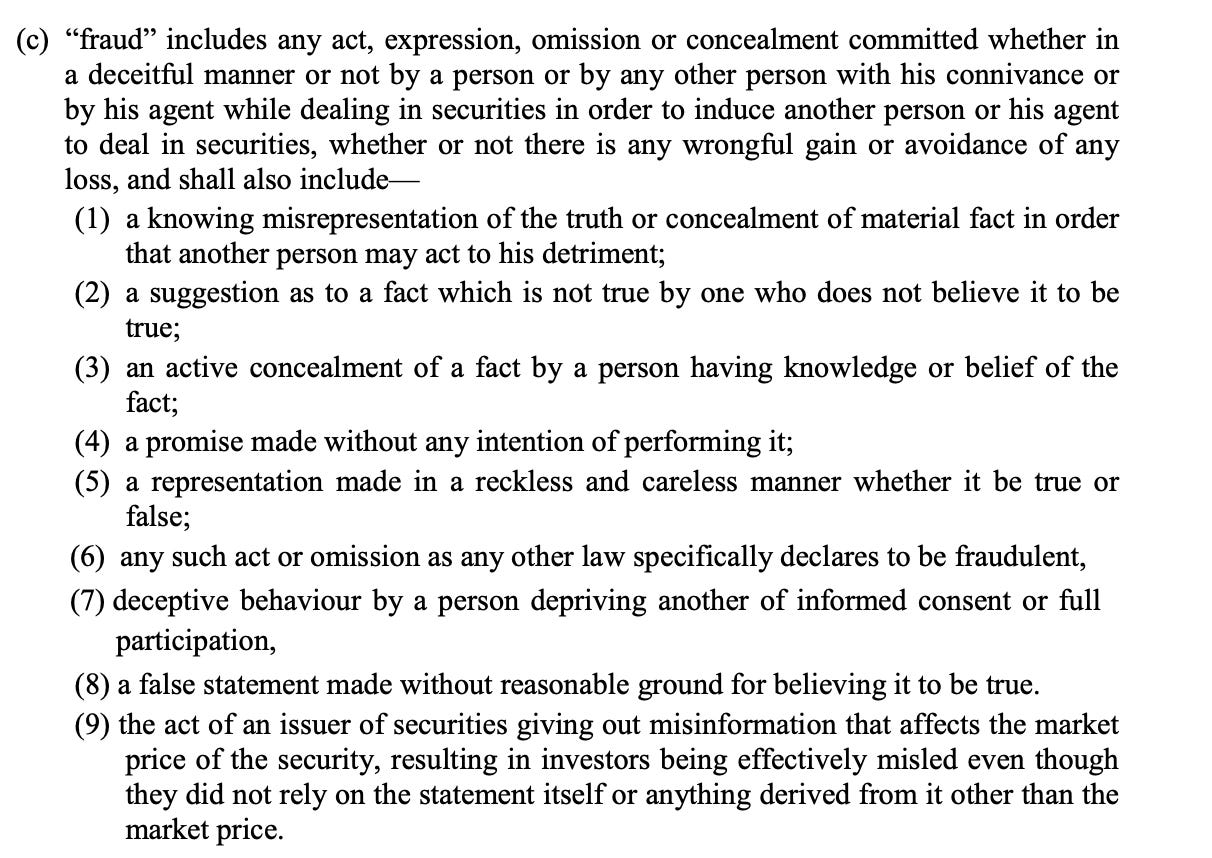

Definition of fraud:

Further, S. 4 dealing with fraud and manipulation is wide and exhaustive. In 4(2) it includes multiple acts deemed to be fraudulent or manipulative. These include any manipulative dealing or fraudulent practice in subscription, artificial manipulation of price, manipulation of benchmark pricing, knowingly spreading misinformation, reckless propaganda, sham transactions without intention to alter ownership, counterfeiting, misuse of funds, circular and wash transactions, churning, forgery, front-running, mis-selling and CIS (Collective Investment Schemes). This is in addition to fraud as defined above. The line between fraud and any other manipulative practice is blurred by using them conjunctively.

The origin of manipulation laws was in fraud[2] because the number of participants in the markets used to be few, and, resultantly, instances of manipulation were also lower. Further, without a digital ledger, a non-fraudulent manipulation of prices was difficult to track. The Indian PFUTP Regulations merge the original doctrinal adherence to fraud with some specific aspects of misinformation to create a wide and hybrid statutory scheme within the umbrella of Fraud and Manipulation without addressing the complications about “ingredients”, “intention” and “standard of proof” requirements as we shall see. The definitions of fraud in the Indian Regulations, for instance, are wider than the SEC’s Code of Federal Regulations[5] definitions: Mere suggestions of fact which are not held in bona fide belief are also included as Fraud. The definition is also wider than definitions in the British Fraud Act[6], where intention to benefit is crucial in all circumstances. The law on securities market abuse has now become much more sophisticated. For instance, the FCA Market Abuse regulations (see the detailed regulations here), transactional specifications of certain prohibited categories of transactions are enumerated in detail[3]. Likewise, in the SEC Code for Federal Regulation, the specific defences against insider trading are expressly codified[4]. When defining fraud in PFTUPR likewise, any “general comment on trends in the securities market”, “criticisms of economic policy” are saved from the definition of Fraud. However, the boundary between a general comment and specific information that can amount to fraud is Indian law is unclear too. Further, because the relation between Fraud and Manipulation is unclear, we do not know if these defences are also available for “manipulation” as against Fraud. PFTUPR makes for a poorly-drafted blanket regulation where all the offending acts are covered in three sections flat. In parts that follow, I only focus on manipulation of scrip price, focusing mostly on “unilateral” manipulations as against collusions.

III. What is Manipulation of Scrip Prices?

Intrinsic valuation by market participants, speculation following from their expectations, opportunism in arbitrage from differing valuations, hedging against risk, inertia from market “trends”, buyers and sellers at a given price and institutional factors shaping all of these are all bundled up into the one number we call price. If that is the case, which elements belong to the “market”, “intrinsic” or “artificial” price? A definitive answer does not exist. Remember that these concepts are only devised to clarify the distinctions between artificial price and other prices.

Let's simplify the idea of a "price" by comparing it to a house for sale. The core challenge for regulators is telling the difference between a normal market price and a fake, artificial one.

The "Intrinsic Price" is what the house is truly worth based on its size, location, and condition. It's the fundamental value.

The "Market Price" is what people are actually paying for it this week. This price includes all the market buzz, excitement, and fear. This is what I have elsewhere referred to alternately as the “true” market price.

An "Artificial Price" is a fake price. Imagine the seller secretly paid his friends to start a bidding war to trick a real buyer into overpaying. That new, inflated price isn't real; it's the result of manipulation. This is also seen and found only through the market, but it is not the “true” market price. It is not the “true” market price in the sense that it comes into being to fraud, deception, illusions which cannot be explained through rational expectations of rational participants formed based on rational assessments of the price. It’s artificiality is an artefact of its incoherence with value, expectations and rationality.

[One may see this post by Samruddha for a theoretical discussion on the various facets of price.]

Roughly speaking, intrinsic price responds only to changes in intrinsic valuation, Market price responds also to expectations and speculation, arbitrage and “emerging” market trends. Artificial price is the price that results from manipulation. Let’s start with that first.

In Jagruti Securities, the SAT determined what constitutes an “artificial price” thus:

“It is axiomatic that a genuine trade will always reflect a genuine price of the scrip…..

We may like to add that the price time priority signifies two things; first is the matching of price and second is the priority in point of time. When a buy order is placed on the system, it will be matched with the best sell order (lowest price) available on the system subject to the condition that no buyer will be made to buy at a price more than what he has offered.... (and vice versa)

If more than one pending buy orders match the sell order, the buy order placed earlier in point of time will be matched first. This is how the price discovery mechanism of the system works as it is based on the free inter play of the forces of demand and supply. The price which the system determines is truly the price which a willing buyer would pay to a willing seller. Once the system has determined the price of a scrip in the aforesaid manner, it can never be described as artificial.

Artificial price, on the other hand, is a price determined by the buyer and the seller in a premeditated manner through collusion by manipulating the system of which we have seen many instances. Black's Law Dictionary (eight edition) defines the word 'artificial' as "Made or produced by a human or human intervention rather than by nature". If we substitute the word 'trading system' for 'nature' in this definition, it becomes clear that an artificial trade/price is the one that is executed or determined by human manipulation rather than through the operation of the system. As at present advised, we are of the view that in an artificial trade there has to be collusion between the buyer and the seller and in the absence of any collusion, the trade cannot be termed as 'artificial'.”

We will have to wrestle with this idea called manipulation to understand what is an artificial price. Is it really that collusion is the only way to manipulate price? No statute defines the manipulation of price.

IV. Some Economic Thinking on Price

The concept of price does not have a concrete meaning and boundary unless we subscribe to a particular theory about how markets function. If the market is efficient, it can value all the information correctly over time, including information about certain deception, fraud and “artificial” manipulation by some participants. The participants just find out and then correct the market by changing their supply and demand. But what about the money that is lost in the interim? The view of the law, however, is closer to mandating (burdening all participants with) “good faith”. It prohibits misinformation, manipulation and fraud. It affords protection to traders if someone created an image that was not the true picture. But is it necessary for them to have believed that image? Is economic loss necessary? We shall see later.

For now, let’s turn to manipulation. Where is the regulator’s bright line on what is manipulative conduct and what is not? No statute defines what constitutes manipulation except by juxtaposing it with fraud.

Secondary markets in scrips thrive on the principle that markets aggregate available information and affect the supply and demand for particular scrips. Through an equilibrium between quantities of supply and demand price is determined. This equilibrium quantity, in fact, arises out of a stable disequilibrium between expectations of buyers and sellers. When sellers don’t want to reduce the offer price and buyers are unwilling to pay a higher price, they don’t concur about changing the price any further, and we arrive at the “market price”. Actionable disagreements of market participants about the price end have subsided for the time being.

All market participants, in addition to their “current valuation” of the scrip, also form expectations about the future movement of the price based on what they deem to occur to the company’s prospects. Speculation, hedging and arbitrage are therefore a usual and necessary part of bearing and dispersing risk in a particular scrip market. By themselves, they do not fall foul of “fair market behaviour.” On a true shared assessment of all its facets, including future prospects, by all the players, we can thus arrive at a “true” market price.

Participants, especially speculators, hedgers and arbitrageurs, make a living by exploiting information gaps in other market participants’ trades and strategising around them. They are under no duty to disclose information they possess. The line between using ignorance and abusing the ignorance of other participants is extremely subjective and thin, and therefore doctrinally difficult to pinpoint. Markets are inevitably unfair to most participants, and avoiding their conflation with an unfair practice by a particular participant is a hair-splitting exercise. When is reliance by market participants on a particular occurrence in a market to alter their trades “unreasonable”, is difficult, too. The market regulator may also have to consider the difference in portfolio size, trading experience and methodological sophistication available to the average trader in making these determinations[9]. Determination of reasonable behaviour for both the alleged defendant and the plaintiffs is based on subjective standards.

One may argue that any “unjustified” or “unreasonable” intentional deviation by a market-player that misleads the market, induces a wrong picture of this “true” price, moves the market away from this true market price to some other market price or prevents return to this “true” market price is manipulative. What even is a “true” market price, now? A market price is a market price, no? As long as the aggrieved participant had all the “public” information at their disposal and they made their own assessments, like the rest of the market, they bear the consequences. What do other participants have to do with it if the aggrieved participants’ assessments went awry?

Note that a “true” market price may be different from the intrinsic price we discussed. True price includes the right kind of speculation, arbitrage, etc. What it excludes is only a change in price that market players have been misled into. It is difficult to guess when the “true” market price and market price coincide and when they do not. What do I mean? Let’s take the dynamic case to understand.

The price of shares is dynamic and changes with time as new information is available about that share or the rest of the market. Not just expectations, intrinsic value may also change as information is discovered. The cash market and the futures market both depend on each other, but that is not necessary. This also means there is no empirical measure of “true” market price or natural price. Like I said earlier, these are conjectural concepts. All we see before us is the market price.

Price is essentially a collection of subjective assessments. What are the proxies of this “true” market price, then? How can I remove all the “noise”?

One way is by remodelling the market and not considering some trades at all to see what the price would have been had those trades not been entered into. But even then, we can’t say for sure if other market participants would have reacted very differently if they had this remodelled information.

Another proxy, for example, is a deflated price averaged over a long period of time. It is assumed that other noisy factors affecting the true market price— the true intrinsic value—average out in the long run. Economists also apply HP filters to get rid of trends and cyclical movements around the “true” market price (they call it detrended averages).

One may also compare the price of this share with the weighted index of prices of other shares in the same sector.

These all may be reasonably good at predicting price changes over a period of time, but are poor proxies of “true” market price at a given point in time. Further, when the market is in a churn, people’s subjective assessment of “intrinsic value” of a thing becomes volatile—they change very fast over a short period of time. “True” market price also becomes volatile alongside “market price” and both are indistinguishable in an extremely liquid market with thousands of buyers and sellers.

Finally, what is the difference between spreading misinformation about a share spread directly and dispersing the misinformation through the market by “manipulating” the market? Is it anything more than the mode of act and therefore the mode of proof? Does it also include the fact that information coming to members “through the market” is more legitimate and that the participants are likelier to rely on it? Should standards for manipulation through the market be lower or higher if it is an effect-based determination? (See footnote 9 below) Are legitimate/ reasonable market practices and manipulation are both to a large extent effect-based, or are they still intention-centric standards? Think about it.

Summarily, the following things emerge from our discussion thus far:

Information is critical to the market process. Information is proprietary, and using information and inferences for one’s own profit is at the heart of markets.

Subjective expectations cannot be aggregated into a “true” market price at a point in time ever all we have are the market prices we see.

Observational equivalence or identification problem means that at any given time, there will always exist more than one causal explanation for market price changes.

One, therefore, can’t empirically tell what the “true” market price at a point is except conjecturally. Which is why there are legal arguments on why something is manipulation or it is not.

Whether the intention of the participant was to manipulate or merely exploit market information to his benefit becomes crucial but can only be determined through inductive inference. Not deductively by looking at the Price Data alone. Intention will have to be imputed by looking at the price data alongside the relevant facts— trade pattern, party involved, etc.

Inducement of a false belief about the “true” market price through unwarranted trades and adverse effect on participants may be necessary.

V. Manipulation continued

Manipulation is therefore defined from the point of view of the actions undertaken by an alleged manipulator. What is unreasonable and otherwise without “legitimate reason” depends on practices that have to be factually ascertained. There is a paradox at play here: One can only infer intention from facts surrounding trades entered and market outcomes. However, we can never be scientifically (>95%) sure of the intention from the facts alone. The law thus assesses claims on the manipulation of a “balance of probabilities”. In light of facts and circumstances.

Manipulative practice is defined in the literature[7] as “profitable trades made with "bad" intent - in other words, trades that meet the following conditions: (I) the trading is intended to move prices in a certain direction; (2) the trader has no belief that the prices would move in this direction but for the trade; and (3) the resulting profit comes solely from the trader's ability to move prices and not from his possession of valuable information.”

What modes of manipulation exist?

The convergence of prices can be unilaterally disrupted in a manipulative fashion by a participant in five important ways: 1) information-based manipulation, 2) trade-related manipulation, 3) cross-market or structural manipulation, 4) market infrastructure and order-placement related manipulation, and 5) multi-player manipulation, aka collusion. Information-based manipulation is simpler to understand. Front-running or insider trading are examples from this category. Order-placement-related manipulation relates to HFTs, etc. I will exclude these in this article.

Let us focus only on trading-related manipulation in 2 and 3. That is manipulation entirely through trades, since that is the case in Jane Street. These unilateral transactions may fall entirely outside the original doctrinal understanding of fraud. A series of transactions is entered into by a participant, and the market relies on the appearance created by these transactions. The line between a permissible transaction and a manipulative one in these cases is thin. Knowledge, purpose and intention of the party in executing the transaction are all the difference between it being a permissible transaction -- entered in merely to stabilise the market[8], regular short-selling, parallel market trades and so forth -- as against a manipulative act. If a transaction is not legally permissible or economically viable, it may often be a finding in favour of manipulation. However, a legally permissible and economically viable transaction by itself does not make it a valid transaction.

In determining these categories of viability and permissibility and the impact of such transactions on the market at large, an account of reasonable market practice is necessary. Often, a transaction may be justifiable as a fair transaction, and in other circumstances, the same transaction may be deemed manipulative. A transaction may even be deviant from a “usual” transaction; in fact, that is what the market rewards, considering the circumstances.

VI. Tentative Facts entering the determination of manipulation

While it is difficult to produce an exhaustive list, a transaction may be manipulative if some or all of the following hold; in any case, these determinations become crucial. The FCA market abuse regulations usefully codify some of these:

1) Any accompanying facts about direct information spread by the participant along with their trading activity.

2) Actual evidence of windfall profits or avoided loss[10], marking the start[11] or close or layering of transactions, proximity of time in buy-sell transactions[12].

3) That without the impugned transactions, it would have been unreasonable for the other market players to act the way they did.

4) Role of the concerned player in the market.[13]

5) Any subset of the transactions could not have led to standalone profits in the ordinary course.

6) If it were a futures transaction, it was singularly and purely speculative and the attending circumstances in the market. LTP of the scrip is relevant[14], so is delivery and losses.

7) Whether there was an impact on the Market (This is, however, rejected as not a necessary factor by the SC in Rakhi Trading[15])

8) Trading at a particular time of the day or repeated arbitrage in a similar transaction and repeated large-volume transactions, volume of liquidity in the trading market by themselves are not manipulative but may create a presumption of manipulation.

9) Derivative contracts in related sector-holdings are affected by volumes in 8).

10) Synchronisation of trades is not per se illegal but may be manipulative in light of other circumstantial evidence.

The courts have to consider the totality of the circumstances in arriving at an inference about whether a particular act is manipulative or fraudulent. That generates plenty of scope for arguments, and it is difficult to reduce this law to doctrinal sophistication. However, we may derive some guidance from decided case laws.

VII. Intention of the Party to Manipulate Price

Some authors argue that without the intention to manipulate the market, there cannot be a satisfactory definition of manipulation at all[16]. Following the doctrinal reliance on fraud, and given that the determination is entirely circumstantial, intention and knowledge play a crucial role in market abuse claims. Intention is a state of mind and can only be inferred from facts. Consider then the two statements below:

Is there enough evidence to infer that the person “actually intended” to manipulate the price?

Is there enough evidence to infer that the person manipulated the market?

Both are to be determined based on the same factual matrix. The question really becomes “was there a design”, or was the price movement “justified otherwise and therefore for a different intention”? But if it was justified otherwise, can we even say that the price was manipulated to begin with? We cannot. Can there even be a uniform standard for these across cash, futures, and options markets across share categories? There cannot be.

Another way to contrast the two statements above is to ask if “there was a design plan” as against “merely accidental” movement of price. But what is the difference between a “merely accidental” movement of price as against “creating a false impression for the market”?

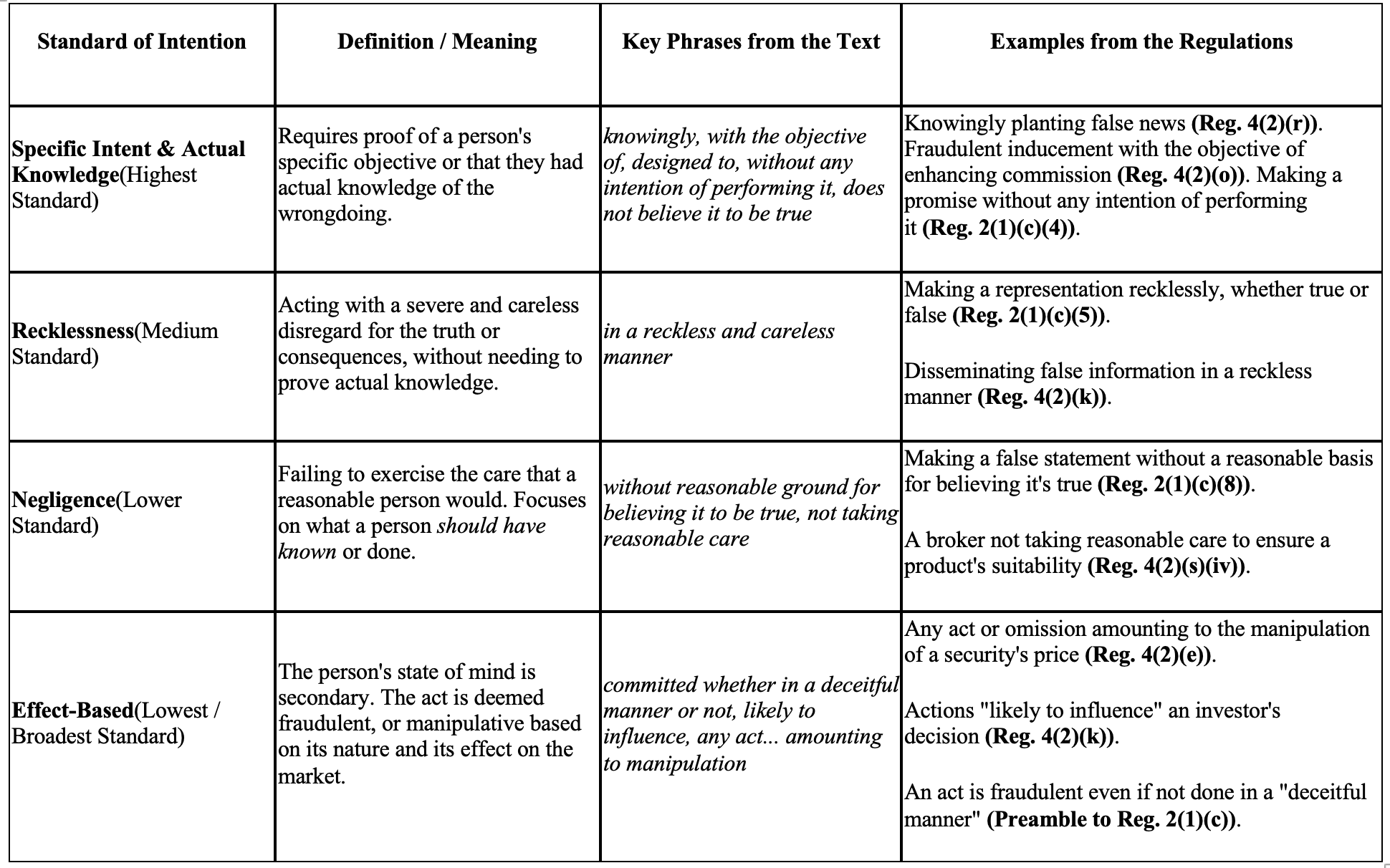

Summarily, is the standard of intention malice — intention to cause the harm that was caused, intention to cause the act that led to harm, recklessness—not taking enough care to ensure that the act that caused harm did not happen, or negligently ignoring knowledge that the acts were likely to manipulate price? All these are standards of intention. Remember that the determination is entirely on facts and on the balance of probabilities.

Is harm—adverse effect on the market— necessary to be proved at all? Can we presume harm if manipulation is established? If harm is not necessary, then is it an “act+intention only” offence? Further, is it necessary to prove that the other traders believed the impressions I had created through my trades to charge me with manipulation?

We enter again the territory of legal determination. Some of these questions are settled, some are not; as we shall see.

The Indian threshold for intention in PFUTPR is very low. It includes reckless propaganda, knowing misinformation, and even knowing or “active” concealment of facts in mis-selling. The standard is also similarly unclear in US law. The law on defence of Scienter and whether deliberate recklessness suffices for a claim of “knowing” fraud, and what standard of recklessness is applicable, is unsettled[17]. Punishing knowing concealment of a material fact is a high burden that hampers the proprietary right of a trader to validly acquired material information, which he may use for arbitrage. This lack of clarity is because the determination is entirely factual to an extent where a coherent body of law has not taken shape.

Deception in section 2(1)(c)(7), for instance, includes not taking informed consent of participants or their full participation. What would that mean in market trades? Am I disentitled from holding any secret information about a particular share? Am I obliged also to publish my inferences while making trades? Does this apply only to directors of a company whose shares are being traded or to brokers to all blanket to participants? The statute does not clarify.

For the manipulation of benchmark indices, the intention of manipulation or knowing acts is not necessary at all. Even manipulation per se is not necessary, and mere “influence” on the benchmark may be sufficient[18]. That is a draconian standard.

The standards of intention and sale for derivatives and futures, as against sale in spot cash markets, have not been distinctly demarcated[19] (the footnote clarifies the position of law), nor are the demarcations of these standards about specific acts of manipulation clear in the statute. This is even when the fundamental motivations of traders in different markets and for different trade designs may be different and may require different threshold standards. It is a jumbled-up regulation.

Let us examine some case law to understand how the courts applied these standards.

VIII. Indian Case Law

Comparator shares and volumes

In Ketan Parekh[20], to examine whether prices of Lupin Pharma had been artificially elevated, the Securities Exchange Board compared its movement with the price movements of other listed pharma companies. The defendants, however, were of the opinion that the size of Lupin Pharma was relatively small and the pace of expansion higher relative to the comparator companies used by SEBI. The SAT accepted the defendant’s argument. Further, the court also examined the volume of transactions as % of total shareholding in Lupin to bolster the conclusion that the transactions were not manipulative. A small player cannot affect the market price on their own. However, volume was not cross-checked with average liquidity in Lupin trades, as even with a small volume in an illiquid market, trades can create false impressions. This is in sharp contrast to Sebi v Ajmera[21], where illiquid scrips were an important factor in rejecting the claim of manipulation. Further, volumes also become irrelevant in some cases, as we will see further.

Lack of Inducement

Another argument in Ketan Parekh was that there was no inducement for other traders because of this artificial price rise. The tribunal first sought to establish whether the price rise in Lupin was “caused” by Parekh and related broker companies controlled by him. However, the court held that ‘inducement’ was a necessary consequence of manipulation and need not be established separately from manipulation. The tribunal observed that the law cannot require the board to discharge an impossible burden of tracking inducement across all public participants in the market. Where manipulation is proved, inducement has to be presumed. If the effect on other traders is not necessary, is an adverse effect on the market necessary? When inducement is necessary to demonstrate effect on the market, the SAT has required showing that the market behaviour was because of the acts of the defendants.

Other intervening factors and burden of proof

In Nirmal Bang Securities[22], the Board had alleged Nirmal Bang of depressing the prices of IT stocks in collusion with some unregistered brokers. However, the SAT held that extant global and national circumstances, like movement in global markets, large selling in the markets, fears of slowdown, financial problems of Ketan Parekh and other such reasons that were leading to a fall in prices had to be considered. If the Board did not admit that the price had fallen because of these factors, SEBI had to prove its version, and mere conjectures would not suffice. The SAT also held that SEBI had to determine “how much of the fall in the price was artificial and how much of it was real and what proportion of the fall can be attributed to a particular person /transaction.”

Correlation and Causation

What the SAT also discussed but failed to apply in its own judgment was that correlation and causation are distinct. In the absence of large volumes of trade, it is difficult to establish an intention to manipulate scrip prices. However, the tribunal held that in the absence of a correlation between the net price of shares and transactions by Nirmal, manipulation could not be established. Here, it is implicit that “showing” adverse impact is necessary and correlation is necessary for causation—both propositions have not been strictly followed by the courts before. Contrast this with the position on adverse impact in Ketan Parekh.

Standard of Proof

The Supreme Court in SEBI v Ajmera[24] reaffirmed that proof under S. 24 had to be beyond reasonable doubt for offences and mere preponderance or probability for civil liability[25] to be gathered by looking at various circumstances read together. The courts before this had been cautious and located the standard between preponderance and beyond a reasonable doubt by merely stating that “mere conjectures were insufficient”, but the standard was concretised at a lower threshold of “preponderance or probabilities” in SEBI v Ajmera.

Which transactions are important for adjudication?

In BP Fintrade[26], the appellant trading company before the SAT, argued that the SEBI had cherry-picked transactions above LTP to make a charge of advance bidding the price. The appellant contended that they had only engaged in momentum trading by taking advantage of the direction of price movement. The volume of trade (10%) was small in an otherwise liquid trade. He contended that trading below the LTP in small volumes did not amount to manipulation ipso facto. There was no evidence on circular trading or collusion, and collusion had not been established[27]. However, contrary to principles established elsewhere and in light of special facts, the court held that small trades below LTP 166 times over multiple days were placed to “create momentum”. 10% of traded volume was a sufficiently significant volume to infer that the trades were inimical to market interests, and such trades below LTP were irrational market behaviour otherwise. The tribunal held:

“it is also on record that in 124 out of 166 times sell orders were placed in single digits of 1, 2, 3 etc shares, which defies the submission of the appellants that they were placing orders below the LTP because only if sell orders are placed a bit below the LTP large quantities could be sold in a falling market. Therefore, clearly the strategy of trading [momentum trading] adopted by the appellants was creating its own momentum inimical to the interest of the securities market. Even if it affected only about 10 % of the market volume in the scrip of Blue Blends, as contended by the appellants, it is no consolation since influencing 10% of the market by 2 entities is a significant deviation from market equilibrium. Therefore, dehors the connectivity issue itself the appellants are in violation of the PFUTP regulations by the very nature of their trading strategy and trading pattern.”

Here, the problem of endogenous causation is the gravest and is insufficiently addressed.

In Kalpana Chedda[28] too, the court similarly had held that where large volumes were available for sale to a mother-son duo, selling a small number of shares over a period of time over LTP was not “normal rational expectations” (they mean rational market behaviour). In aggregate, they manipulated the market as top-two net sellers while offloading the shares towards the tail of the transactions at a higher artificially inflated price.

Along similar lines, in Shri Nagad Sarvar v SEBI, the fact that he had executed only buy trades and only sell trades on some days and had also made losses on a few days was relevant in holding that his behaviour did not lead to manipulation of scrip prices. The court held that where the appellant had occasionally gotten beneficial ownership by taking delivery, his parallel buy and sell trades were not matched within short periods, it could not be held to be a wash trade, and it was, in fact was a legitimate transaction. However, the standard was very different in BP Trading, where different trading patterns afforded no relief. There, the court held that”

“A large number of sell orders were placed repeatedly on several trading dates at less than the LTP; it is illogical …. Of course we notice that a number of orders of the appellants were placed on or marginally above LTP, but that is the rational behaviour expected from a seller and no fault can be found for SEBI in not considering such trades as violative of the PFUTP Regulations.

Appellants’ submission of a small list of trades in which they impacted LTP both positively and negatively on a few days also does not help the appellants since the overwhelming evidence is clearly towards placing sell orders below the LTP.”

Collusion

In the Kalpana Chedda case, the SEBI had never analysed the buy-side of the shares, only that the seller had sold them above LTP. Therefore, any evidence of collusion could not have been produced. However, the tribunal did not order a reinvestigation. There was no collusion in Saumil Bhavnagari[29] either, only the fact that the advance bid often was the first trade of the day, above LTP, which, according to the SAT, was made to influence prices.

These two cases must therefore be distinguished from another line of small-share-selling cases where it was held that to establish manipulation by advancing bids, is to be proven for trades above or below LTP, proving collusion between buyer and seller was necessary. In Nitish Shah HUF[30], too, the court upheld the proposition that without such collusion, no causal relation between trades and manipulation could be established. In the absence of any relation between the buyer and seller, the mere selling of small quantities around the LTP was not manipulative[31]. Here, too large buy orders were available when small orders of 25 shares were placed, but that was not considered by the court. Further, the fact that the appellant was trading all other scrips in large quantities, unlike this one, was also not considered. Another question that begs attention is whether collusion is irrelevant where the SEBI has not alleged any collusion, but relevant only where SEBI alleges but fails to prove collusion?

Circuit Limits

One other crucial characteristic in price-manipulation cases considered by the tribunal was the circuit limit[32], where the court observed that trades within the circuit limit (in the absence of an LTP buy/sell offer that is pending) were permissible and did not lead to an inference of manipulation. This had also been a factor in Jagruti Securities before the AO[33], but the AO drew an adverse inference of the fact that the trades were close to the upper circuit.

As we can briefly see throughout this discussion, the weight attached to different contributing factors in cases of unilateral manipulation of scrip prices is uncertain and often incoherent. The multiplicity of circumstances with uncertain weight and the use of the preponderance of probabilities as a standard of proof may lead to conflicting guidance. The courts, too, have urged for an advanced and nuanced framework on manipulation[34]. Indian case law has advanced substantial criteria and considerations for determining manipulation independent of the weight ascribable to them. Let’s apply these standards to the Jane Street Case.

IX. Jane Street Group Interim Order

In the Jane Street matter, all the issues discussed thus far come into sharp contrast. The interplay between the derivate and the cash market, standards for index option trades, close-to-expiry trades, profit and loss patterns, correlation of prices with trading activity, volumes of trade, buying above or below LTP in liquid markets without collusion of any sort, LTP movement, market impact, concurrence of activity, relevant comparison groups, continuing negligence and disregard for regulatory caution, economic rationale, legal permissibility, extended marking of the close, impact on market participants, use of position of self and associated players.

Jane Street purchased heavy volumes of the component shares of BANKNIFTY in the cash market and futures market. Since FPIs cannot execute intra-day trades, Jane Street executed them through its Indian subsidiary. As the prices in the cash market were supported, other participants in the options market followed suit by taking long positions early in the day. Jane Street, however, took short positions early in the day. Towards the end of the day, they closed positions in the cash market at a loss. However, since the options market is much more liquid and had a notional turnover was over 353 times the cash market turnover, the absolute volumes and profits booked in the options market through the crash induced by their sale in the cash market were much higher.

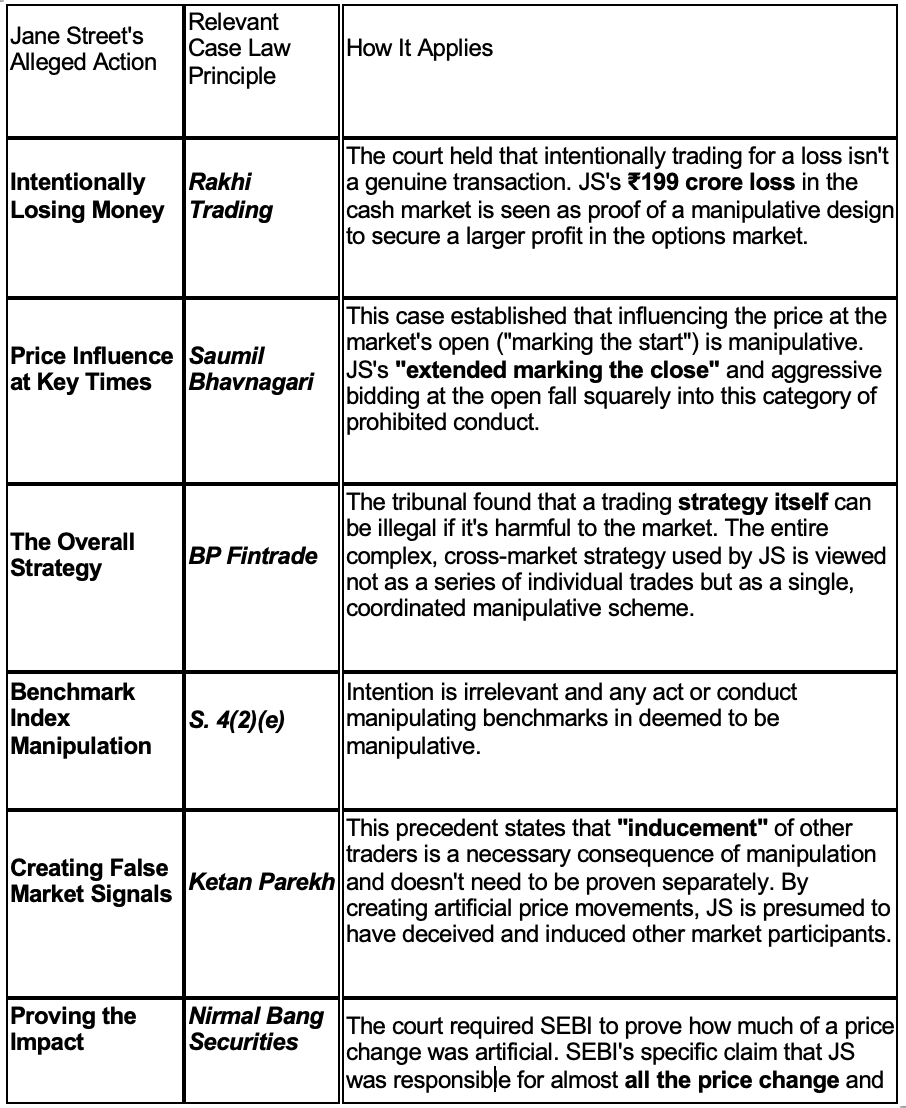

The SEBI interim order, which is a factual order, covers all actors considered hitherto and enunciated above in this post. Since index prices form the “benchmark” for trading in that sector, any act of omission, irrespective of intention, is sufficient to hold that it is a manipulative practice. Further, JS engaged in extended marking the close on 3 days. Extended marking of the closing price is considerably influential in determining manipulation. Jane Street incurred a deliberate loss of 199 crores in the Cash and futures market across 15 days, which is inexplicable otherwise and falls foul of the test in Rakhi Traders. It is unclear whether they made losses in the cash market on all days, as the SEBI interim order does not point to that. This could turn out to be in JS’s favour in the final report. The SEBI has added that almost all changes in price in the cash market were driven by the trades undertaken by the JS Group.

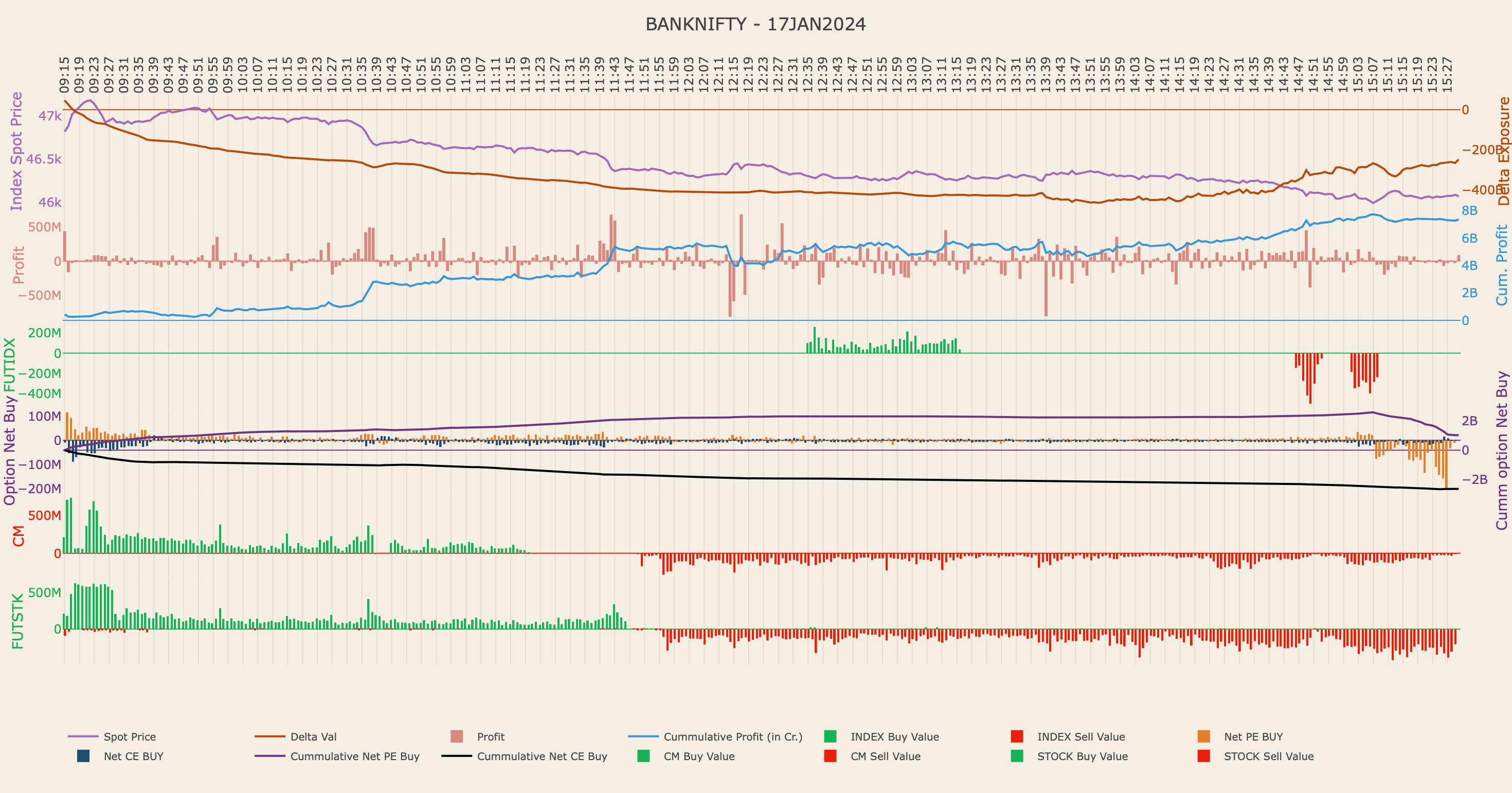

Precise allegation - The 17th January Trades

See the chart here. See the net value of purchases/sales in Cash Market (CM) and Futures Market (FUTSTK). Also see the change in Delta exposure through the day.

Jane Street in the early minutes of 17th January aggressively pushed the LTP by bidding at LTP or above LTP to counter the substantially negative market sentiment that day. The SEBI estimated JS’s contribution to LTP was as much as double of what the scrip price would have been otherwise. We do not know how SEBI has arrived at that number, but it could be challenged. The note says: “The LTP impact attributable to the rest of the market was computed by adjusting the total price movement (vis-à-vis the respective scrip), for the impact created by Jane Street’s trade.” However, in law, this finding of the precise effect of Jane Street’s contribution to price manipulation is consistent with decided case law.

Jane Street could argue that its move was directed at stabilising the market, given the circumstances, but given other circumstantial evidence, it is unlikely to sustain because the firm also simultaneously acts in the options market. As the market expected the momentum to sustain, call options became expensive and put options became cheaper. JS sold call options, which became expensive, and bought put options that had become cheaper to take a bearish position in the options market. This makes no economic sense unless one has a strong reason to believe that the momentum they have created will not sustain. It could be argued that we tried to sustain the momentum but could not, and therefore resorted to selling our positions. However, the delta exposure was built consistently since the start of the day and the puts were exercised very close to the end of the day, starting at 3:15. (See chart above)

The volumes in the cash market were substantial 15-25% volumes in each bank. (Refer to the report for precise numbers) Further, the options volume cash-equivalent was INR 32,114.96 crores in short positions in BANKNIFTY via index options, in absolute terms, was 7.3 times the INR 4,370.03 crores long position built by the group aggressively in the component cash/ futures markets. Then, in the intra-day market, JS aggressively sold its positions and booked losses in the cash market. However, it profited much more in the options market. This modus operandus was run on 15 days. The impact on both the cash and options markets was substantial, as it amounted to deception of the players to alter “normal” market prices. The fact that it was done through a subsidiary to bypass the FPI intra-day regulations is also significant.

X. Legal Position qua Jane Street Allegations

While I have borrowed individual propositions from particular cases to show how they have been covered, the overall case has to be collectively considering all facts and circumstances. Jane Street may argue that their transactions early in the day were to hedge against other portfolio risks, and they therefore were constrained to sell. They could also argue that their positions in the Futures market were consistent and were reversed on account of some information, including the market trends reversing independently of their activity. Further, they tried to provide support to the index till 11 am to stabilise the market. However, they were unable to support the index and had to reverse their strategy. The coincidence in timing was because of a genuine reversal of strategies.

However, aggressive momentum-support positions in the cash market are exactly opposite and simultaneously taken with short positions in the options market. Both cash and options positions were closed with a reversal of the trading strategy at the end of the day. Taking such positions repeatedly makes no market sense, and they are extremely risky positions for any reasonable trader who knows he cannot influence the market on his own. It is extremely difficult to explain this as a complex arbitrage.

It is unlikely that the defences will survive on the preponderance of probabilities in any case. Further, there are judgments to the effect that if the negligence is continued, standards for intention are relaxed. The fact that the manipulation continued even in the face of notice from SEBI about unjustifiably high delta positions in the options market could be considered continuing negligence. Overall, the SEBI has a strong legal case, consistent with the way law on manipulation has evolved in India, and it is unlikely that Jane Street will succeed in its defence before the SAT on the merits. The case is slotted for hearing today in the SAT and would be definitive in understanding the contours of cross-market trades and standards for options trading.

[1] As Amended in 2024

[2] Regulation of Stock Market Manipulation - Comment, Spitzer et al. Yale Law Journal (1946-47). The history of manipulation law is also detailed in Regulation of Manipulation Under Section 10(b): Security Prices and the Text of the Securities Exchange Act of 1934, Steve Thel, Colombia Business Law Review (1988)

[3] FCA Market Abuse Regulation 6.6

[4] SEC CFR on Market Regulation. Also, in 10(b) of the SEC Act, 1934

[5] 17 CFR 240.10b-5

[6] Fraud Act, 2006, UK Parliament

[7] Daniel R. Fischel & David J. Ross, "Should the Law Prohibit 'Manipulation' in Financial Markets?," 105 Harvard Law Review 503 (1991).

[8] The UK and the USA recognise stabilisation as an 'acceptable' type of market manipulation, whereas the German regime is silent on this point. Lomnicka (2001)

[9] In the Ketan Parekh case: “Tragically, retail investors and day traders are most vulnerable to such trading as they follow the herd mentality because they lack market intelligence and experience to diagnose such cases, and they are usually the ones left holding the parcel when the music stops. Also, in Nishith HUF v SEBI, “It must not be forgotten that ..may influence the innocent/gullible investors”

[10] Nobody intentionally trades for a loss. An intentional trading for loss per se is not a genuine dealing in securities in Rakhi Trading

[11] Saumil Bhavnagari vs Sebi on 21 March 2014, where the proprietor for 85/175 orders placed most orders first in the day, higher than LTP, and claimed that he was positive about the financials of the company. This defence was rejected by SAT even in the absence of any collusion.

[12] In the US, the size of profits is not relevant

[13] SEBI has not bothered to distinguish between client sales and proprietary sales in Nirman

[14] Jagruti Securities holds, “It is axiomatic that a genuine trade will always reflect a genuine price of the share.”

[15] A position not followed in Shri Nagad Sarvar v SEBI, where the tribunal inter alia held that the board had not demonstrated an adverse effect on the market.

[16] Fischel and Ross (1991)

[17] Matrixx Initiatives, Inc., et al. v. Siracusano et al. 563 U.S. 27 (2011) Certiorari to the United States Court of Appeals for the Ninth Circuit No. 09–1156. Argued January 10, 2011—Decided March 22, 2011.

[19] The Supreme Court rejected such an argument made in Rakhi Trading. This had been the logic of the SAT order where the SAT held: “when Nifty is traded in options contracts, the movement of prices in that segment cannot have any impact on the price discovery system in the cash segment which is one of the allegations” The SAT argued that in the future options contract reversal of contract was to be treated differently from the cash-market because in derivatives the underlying security may not be intended to be transferred at all. The SC, however, rejected this argument.

[20] Ketan Parekh vs Securities And Exchange Board Of India on 14 July 2006 SAT

[21] 2016 (6) SCC 368

[22] Nirmal Bang Securities Pvt. Ltd. vs The Chairman, Securities And Exchange Board on 31 October, 2003 SAT

[23] Sterlite Industries (India) Ltd. vs Securities And Exchange Board Of India on 22 October, 2001 SAT

[24] supra n 22

[25] Reiterated in Rakhi Trading

[26] Bp Fintrade Pvt. Ltd. vs Sebi, SAT, 20 November 2020

[27] As in Jayendra Chandulal Sheth SEBI order 2019, also in Moneygrowth v SEBI 2008

[28] Mrs. Kalpana Dharmesh Chheda vs Sebi on 25 February, 2020 SAT

[29] Saumil Bhavnagari vs Sebi on 21 March, 2014 SAT

[30] M/S Nishith M. Shah Huf vs Sebi on 8 January, 2020 SAT

[31] Reliance was also placed on Jagruti Securities in addition to Ajmera

[32] In Jagruti Securities, the parties were trading small to avoid the upper circuit.

[33] Adjudication Order No. AP/AO-20/2005-06, Paragraph 4.15

[34] Rakhi Trading, Ajmera, Kannaiyalal Patel SC 2014